Only a small number of crypto enthusiasts knew what non-fungible tokens (NFTs) were at the start of 2021.

But it’s not taken long to change that, with nearly $41bn being spent on NFTs this year, making the digital artwork and collectibles market nearly as valuable as the global art market.

But what are NFTs?

NFTs are cryptographically unique digital tokens which prove ownership of physical or digital content such as art or land.

They’re essentially digital ownership certificates registered on a blockchain – an unchangeable record that can’t be tampered with.

The tokens are usually created or minted using smart contracts and are then traded on the secondary market in exchange for cryptocurrency.

The NFT collectibles frenzy first began in 2017 with the launch of the CryptoKitties game and the demand for these digital cats.

At its peak, the blockchain game had 140,000 daily users and 180,000 daily transactions in November 2017, but this traction was quickly lost over a few months.

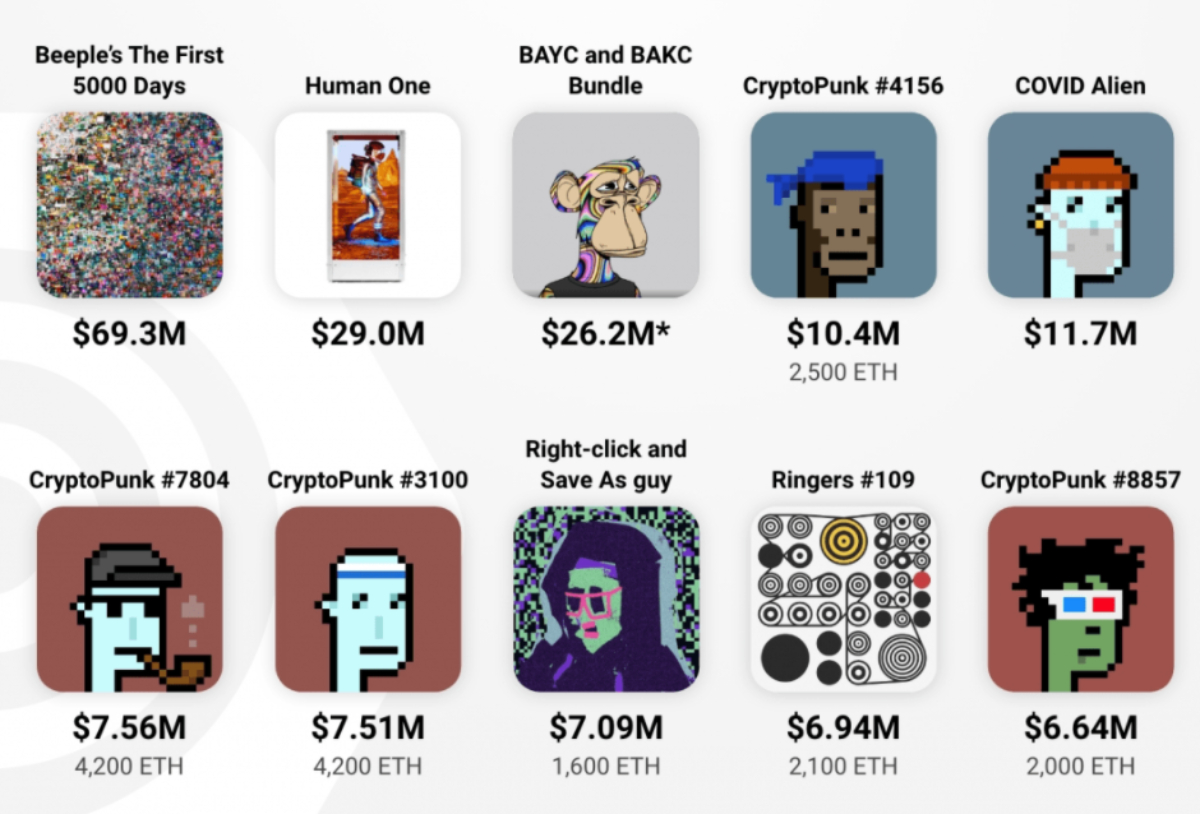

NFTs then really became mainstream in March 2021, when a collage by artist Mike Winkelmann – known as Beeple – sold for $69.3m at Christie’s.

This was the first sale of its kind at the auction house.

Although NFTs were first popular in the art world, world renown corporations, sports leagues and celebrities have embraced them to cash in on the surge in interest.

The NBA created its own NFT marketplace for buying, selling and trading video highlights of its players called NBA Top Shot.

NFL star Tom Brady launched a sports NFT platform which sells signed NFTs in retro 8-bit style.

Kings of Leon released its latest album as an NFT, which includes gig tickets.

While collections such as CryptoPunks and Bored Ape Yacht Club have gone viral and formed online communities, being used as avatars on social media profiles by celebrities and influencers including Snoop Dogg and Jimmy Fallon.

CryptoPunks changed hands in 2019 for anywhere between $60 and $600, the same punks then traded between $600 and $3,500 in 2020.

But, in 2021, those exact same CryptoPunks traded for prices between $480,000 and $1.25 million.

Visa joined the hype and bought a CryptoPunk for $150,000 in summer 2021.

Facebook then rebranded to Meta on October 28 in a bid to expand its reach beyond social media and into the metaverse.

Longer term, enthusiasts hope NFTs will one day power ecommerce in the metaverse or metaverses which will be virtual worlds filled with digital avatars.

In the metaverse NFTs could prove ownership of virtual goods, such as land, clothing, cars etc.

In the last week of October, it was revealed over $106 million worth of virtual land was sold as NFTs.

While Nike announced it had bought a virtual shoe company to mint virtual sneakers.

The ‘GameFi’ industry also boomed in 2021.

GameFi is defined as the combination of gaming and decentralised finance (DeFi).

The leading game has been Axie Infinity followed by the likes of Decentraland and The Sandbox.

Axie Infinity is a game where players collect Axies as pets in order to battle, breed, raise and build kingdoms for their pets.

The game ecosystem is powered by cryptocurrencies AXS and SLP.

The Axie Infinity collection has quickly risen to become the most traded NFT collection ever in the short history of NFTs thanks to the hype and has had nearly $4 billion in all-time sales.

In total, according to Chainalysis – a crypto analytics group – $40.9bn has been spent on Ethereum blockchain contracts which are typically used to create NFTs in the year to December 15.

The total would be much higher if it included NFTs minted on other blockchains, such as Solana.

In comparison, in 2021 the global art market was worth $50.1bn, according to figures from UBS and Art Basel.

Chainalysis also small transactions of under $10,000 accounted for over 75 per cent of the market, but much like cryptocurrency, it remains dominated by a few “whales”.

Between late February 2021 and November 2021, there were 360,000 NFT owners holding 2.7 million NFTs.

Of those, only 9 per cent (32,400 wallets) held 80 per cent of the market value.

NFT investor, known as Pranksy on Twitter, started with an initial investment of $600 in 2017 and now has a portfolio worth more than $20 million.

But according to blockchain analysis platform Nansen most new NFT collectors on the secondary market are yet to have recuperate the costs of their purchases.

While early investors have benefited from a rise in the price of the NFTs as well as the cryptocurrency used to trade them.

The NFT space has also been a hot spot for fraud, scams and market manipulation.

Analysis by Nansen found $2 million of suspect activity across the CryptoPunk and Bored Ape Yacht Club collections from mid-November to mid-December alone.

Some were sold at a 95 per cent discount to their estimated value, either because of mistakes by buyers and sellers or tax write-offs.

Tax agencies such as the Internal Revenue Service are yet to address NFTs directly, but some believe they could be deemed “collectibles” and subject to capital gains taxes.

Some also believe the market is being inflated by wash trading – this is when a trader sells and buys the same asset to give a false impression of demand.

But despite this there are plenty of people who believe the market will continue to evolve and offer a number of features, such as allowing artists to collect royalties forever.

2021 was a year of unimaginable growth for the NFT space.

But could 2022 top this?